How to Choose the Right Life Insurance Policy in the U.S

Understand the key differences between term and permanent life insurance policies, and learn how to choose the best option for your financial goals and family’s future.

Why Life Insurance Matters

Choosing the right life insurance policy in the United States is one of the most important financial decisions you’ll ever make. It's not just about covering final expenses—it’s about protecting your family, ensuring long-term financial stability, and creating a legacy. But with so many policy types, providers, and fine print details, making the right choice can feel overwhelming. This guide will help simplify the process so you can make a confident, informed decision.

Understanding the Purpose of Life Insurance

At its most basic, life insurance provides a lump-sum payment, called a death benefit, to your beneficiaries after your death. This money can be used for funeral costs, mortgage payments, college tuition, or simply to maintain the family’s standard of living.

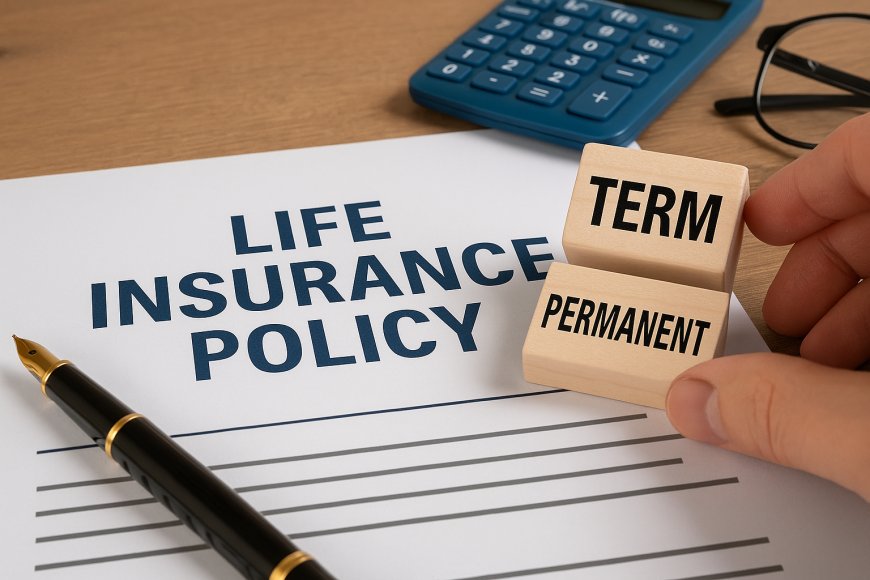

Term Life vs. Permanent Life Insurance

There are two main categories of life insurance policies in the U.S.: term life and permanent life. Each has its advantages and drawbacks, and your choice should be based on your goals, age, income, dependents, and financial obligations.

What Is Term Life Insurance?

Term life insurance is often the most straightforward and affordable option. It covers you for a set period—typically 10, 20, or 30 years. If you die during that time, your beneficiaries receive the death benefit. If you outlive the term, the policy expires with no payout. Because term policies don’t build cash value, they’re generally cheaper and ideal for younger families or those with limited budgets.

What Is Permanent Life Insurance?

Permanent life insurance offers lifelong coverage and typically includes a savings or investment component known as cash value. This category includes whole life, universal life, and variable life insurance. Whole life provides fixed premiums and guaranteed cash value growth. Universal life offers flexible premiums and cash value growth based on interest rates. Variable life allows you to invest the cash portion, potentially growing your benefit—but with more risk.

Considering Costs and Budgets

Term life is significantly more affordable, especially for healthy individuals under 50. Permanent policies cost more but can serve as long-term financial tools, offering tax-deferred growth and even income during retirement. However, they require a bigger financial commitment and careful planning.

Tailoring Coverage to Family Needs

If you have young children, a mortgage, or large debts, a term policy might offer enough protection affordably. If your goal is to leave behind wealth, ensure lifelong coverage, or provide for a dependent with special needs, permanent life insurance may be worth the added cost.

Do Employer Policies Cover Enough?

Employer-provided life insurance is usually limited to 1–2 times your salary and may not be portable if you change jobs. It’s smart to supplement this with your own policy, ensuring long-term protection that isn’t tied to your employment status.

Choosing a Reliable Insurance Provider

Not all insurance companies are created equal. Look for those with strong financial ratings (A or better) from agencies like AM Best or Moody’s. Read reviews, compare quotes, and consult a licensed broker to help guide you toward a trusted carrier.

What to Expect During the Application Process

Applying for life insurance usually involves a health exam, background checks, and questions about lifestyle and finances. Some companies offer no-exam policies, but these often have higher premiums or lower coverage. Always be honest—false information can invalidate your policy.

How Much Coverage Do You Really Need?

To estimate your needed coverage, consider mortgage debt, income replacement, children’s education, and final expenses. Many experts recommend 10–15 times your annual income as a starting point, but your unique life stage and responsibilities may require more or less.

When to Review and Update Your Policy

Review your life insurance annually and after any major life event—like getting married, having children, or buying a house. As your responsibilities shift, so should your coverage.

Additional Tips for Smart Policy Shopping

Don’t delay purchasing life insurance—rates increase as you age. Be cautious of high-fee bundled plans that combine investment elements you may not need. Prioritize transparency and simplicity in both costs and coverage terms.

Final Thoughts

Choosing the right life insurance policy in the U.S. comes down to aligning your policy with your financial goals, family structure, and future plans. Whether term or permanent, the best policy is one that offers peace of mind—today and for the people you care about tomorrow.