All-in with Hawaiian Airlines Miles: Better late than never? [2-card option is dead]

Last year, Greg went all-in on Hawaiian Airlines Hawaiian Miles. At the time, I hesitated. I really can’t explain why it took me so long, but I’ve finally hopped on board the Hawaiian Airlines Hawaiian Miles train. Unfortunately, waiting to do so means that my bet on Hawaiian isn’t as good as Greg’s was. Is […] The post All-in with Hawaiian Airlines Miles: Better late than never? [2-card option is dead] appeared first on Frequent Miler. Frequent Miler may receive compensation from CHASE. American Express, Capital One, or other partners.

![All-in with Hawaiian Airlines Miles: Better late than never? [2-card option is dead]](https://frequentmiler.com/wp-content/uploads/2025/04/wp-17453569768231422404920437706643.jpg?#)

Last year, Greg went all-in on Hawaiian Airlines Hawaiian Miles. At the time, I hesitated. I really can’t explain why it took me so long, but I’ve finally hopped on board the Hawaiian Airlines Hawaiian Miles train. Unfortunately, waiting to do so means that my bet on Hawaiian isn’t as good as Greg’s was. Is it time to go all-in for real, or is it too little too late?

Why the big interest in Hawaiian Miles?

In short, Hawaiian Miles became interesting when Alaska Airlines bought Hawaiian Airlines last year and made known their intentions to merge the two airline programs. Whereas Hawaiian Miles have historically been of limited use, Alaska Mileage Plan miles are highly valuable. As things stand, it is possible to move Hawaiian Miles to Alaska miles on a 1:1 basis. The programs are expected to combine into a single loyalty program in the coming months (Alaska has long pointed to “Summer 2025” for the final program merger).

It is widely expected that when the merging of programs is complete, opportunities to earn “Hawaiian Miles” will likely disappear. The Hawaiian Airlines credit cards and transfers from American Express Membership Rewards to Hawaiian will most likely end this summer. It is important to note that it hasn’t been confirmed when those things will cease to exist, but Alaska has been clear that they are not interested in maintaining transfers from Amex and they they are happy with Bank of America as their credit card partner (Barclays issues the Hawaiian cards). We are very likely in the final months of those opportunities to earn Hawaiian miles.

While Alaska miles are highly valuable, they are much more difficult to earn through credit cards. Bank of America has long issued just two Alaska Airlines credit cards, a consumer card and a business card. Both cards offer just 1 mile per dollar on most purchases and intro bonuses on those cards have never been huge. A premium card is expected this summer, but we don’t yet know what to expect. Alaska partners with Bilt Rewards, so those collecting many points via Bilt do have that avenue by which to collect miles through rent, Bilt Dining, Lyft, Walgreens, and the Bilt Rewards credit card. However, with only one Bilt credit card currently on the market and no welcome bonus offered on that card, collecting a meaningful number of Bilt points is an exercise in patience.

By contrast, Hawaiian has 3 credit cards on the market (two consumer and one business) and is transfer partners with American Express Membership Rewards. That means there is significant opportunity to collect Hawaiian miles in ways that will likely end within the next few months, thus the interest in picking up miles where possible.

In my household, we’ve both been collecting Hawaiian miles and Membership Rewards points lately with an eye toward building up a balance on the Hawaiian side, combining our miles, and having a nice stash built up with Alaska before it once again becomes difficult to collect many Alaska miles.

Applying for two Hawaiian Airlines consumer credit cards in one day

I recently realized and highlighted the fact that there are two Hawaiian Airlines consumer credit cards and that it is possible to be approved for both of them on the same day. I had previously thought that one had to be a Hawaii resident to apply for one of them, but I learned that wasn’t true and I put the process to the test myself.

The two consumer cards are the Barclays Hawaiian Airlines World Elite Mastercard and the Bank of Hawaii Hawaiian Airlines World Elite Mastercard. While the second card in that sentence is marketed as a “Bank of Hawaii” card, both credit cards are actually issued by Barclays. The good news is that these cards are treated as separate products, but you’ll need the help of a human to get past a computer system that isn’t built to recognize that.

In my case, I filled out the applications for both the Barclays and Bank of Hawaii cards simultaneously, advancing page by page through the applications in two browser tabs at the same time. I had the opportunity to select card art during the process and so I chose different card art for each application in order to be able to identify the cards later at quick glance (or to identify which card I was calling about if I needed to explain things to a representative, but that wasn’t necessary).

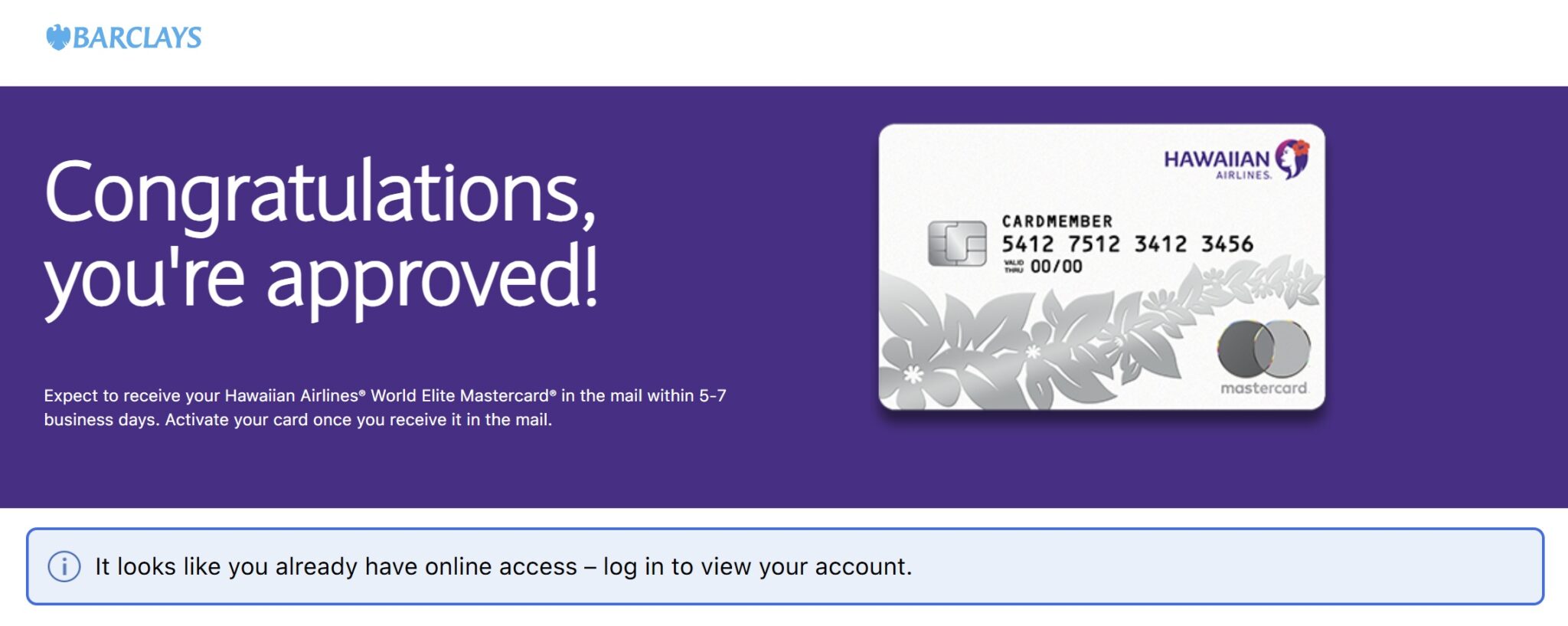

I submitted my application for the Barclays version first. It was instantly approved.

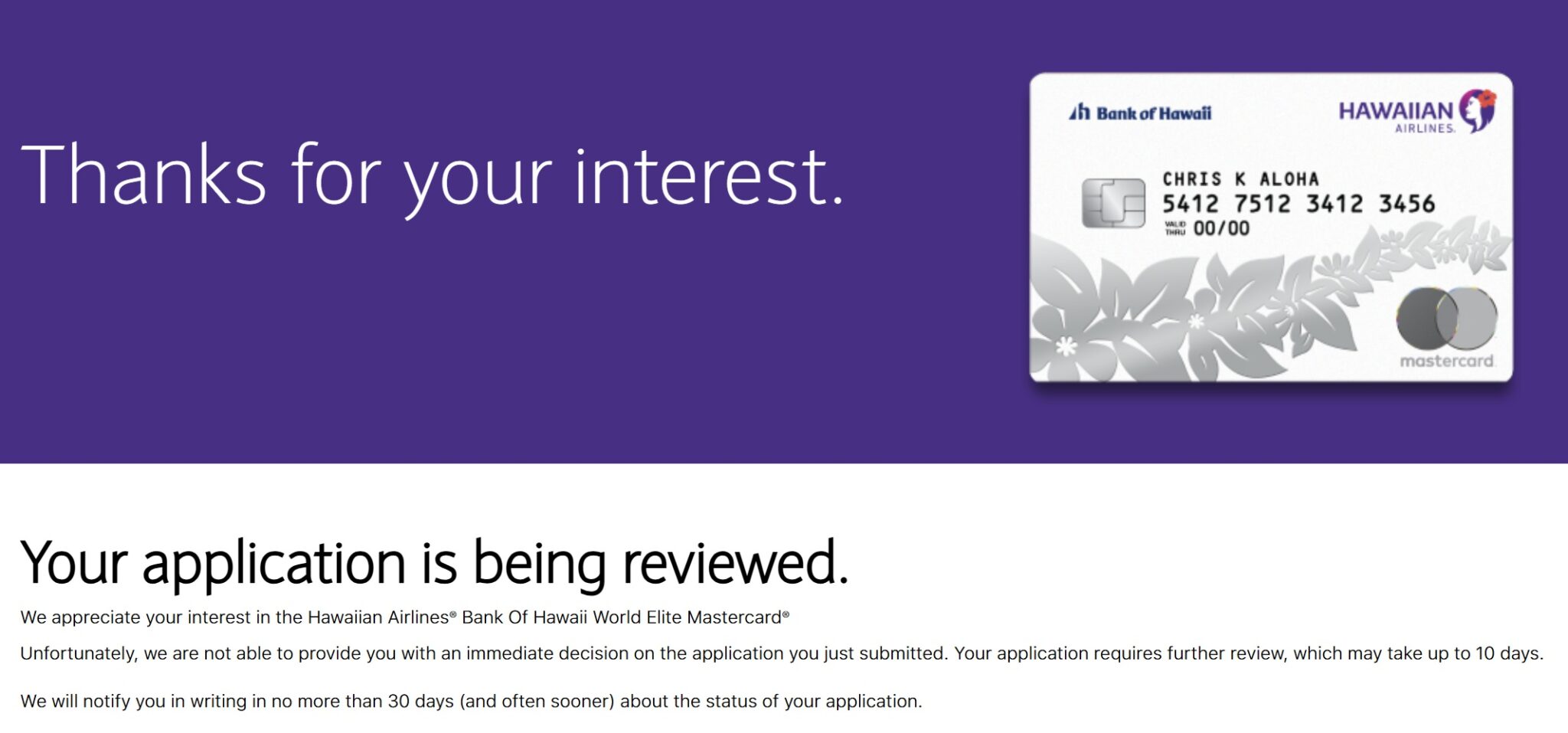

I then immediately clicked “submit” on the Bank of Hawaii-branded application.

As expected, that second application was not instantly approved but rather said that the application was being reviewed. Existing cardholders of one of the cards who apply for the other version often report receiving a screen indicating that they already have a Hawaiian Airlines credit card rather than the above “under review” screen.

In either case, the next step is to call Barclays reconsideration at (866) 408-4064 (note that the phone number for reconsideration is listed on all of our card pages). I believe the reconsideration department is open until midnight Eastern time on weekdays. When a representative answered my call, I explained that I had submitted a credit card application that wasn’t instantly approved and was wondering whether there was anything I could do to help.

The rep verified my personal information and could see the applications. She started to say that she could see that my application wasn’t processed because I “already have…” before stopping herself mid-sentence to say that she sees the second application was for the Bank of Hawaii version of the card. From what she said, it sounded like the computer system isn’t set up to consider the cards separate products, but representatives are aware that they are. She asked if I’d like to have her process that second application. When I confirmed, she read some disclosures and then asked me some questions about my expenses. She asked if I would be willing to move credit line from the new Barclays-version Hawaiian card or another of my Barclays cards to the Bank of Hawaii card. I was totally willing to do that. Since the spending requirement on the Bank of Hawaii version is only $2,000 in 90 days and since I didn’t need a high limit on it, I asked to move just $2,000 from my new Barclays Hawaiian card to the Bank of Hawaii version.

She told me that the application was approved, but upon further review she said I would need to verify some identity information with a team that was only available between 8am and 8pm (I was calling after 8pm). She gave me the number and I intended to call the next day. However, I soon saw both Hawaiian Airlines credit cards in my Barclays login. Interestingly, I initially saw the $2,000 shift in credit limit, which is to say that my Barclays version showed a credit limit that was $2K less than the initial instant approval since I had moved the $2K to the Bank of Hawaii card. However, a day later, the credit line on the Barclays version of the card had increased back to the initial approval amount and my Bank of Hawaii card maintained the $2K limit, so it seems that they determined that I didn’t need to move credit for a small line like that.

I’ve since received and activated both cards. I never called the department that she said would verify my information since everything just showed up automatically.

Many blog readers, Facebook group members, and podcast commenters have succeeded in getting both versions of the card. A couple of days ago, one reader reported being told by a representative that it was no longer possible to apply for both cards, but she later called again and was approved. In her case, she had previously held the Bank of Hawaii version of the card for 6+ months. When she applied for the Barclays version, she received the messaging saying that she already has a Hawaiian Airlines card. When she called, the first representative she reached indicated that while some customers had been approved for both, the two credit cards are really the same product and as such they wouldn’t continue to approve applicants for both (and they didn’t run her application on that first call). I advised her to call again and see whether she got the same answer or had just gotten a misinformed representative (which happens in many cases in the miles and points world). Sure enough, the second time she called, her application was processed and she got the card.

In the collective reports I’ve seen, the vast majority of reconsideration reps seem to proactively recognize that these are separate products, so if you get one that says otherwise, it is probably worth a follow-up phone call.

Unfortunately, I dragged my feet on these offers long enough to have only gotten in for a welcome bonus of 60,000 miles on each card. Both cards previously offered 70,000 miles (and the Barclays version is back out with a 70K offer now!).

My wife recently got the Barclays Hawaiian Airlines Business Mastercard and completed the spending requirement and earned the welcome bonus. Her bonus was only 50,000 miles.

All three were low offers. I regret not applying for these cards while they all featured increased offers! That said, I am glad to have gotten these cards while they are still available. While not as good as it could have been, we’ll earn 170,000 valuable miles on the three cards we’ve opened. We expect that these cards will likely no longer be available in the not-very-distant future, so we were glad to get in while we could.

I’ll add that we don’t know what will happen with Hawaiian Airlines cards once the merger is complete. I don’t know whether they will become Alaska cards or end up product changed into something else or what, but I was happy to get my collectibles while I could.

Upping the ante with Amex Membership Rewards

![]()

Thanks to a pretty robust set of family trips this year and early next year, I’d heavily depleted my American Express Membership Rewards stash by the beginning of 2025. I’ve been working at replenishing those points over the past few months through a new card bonus, targeted employee card bonuses, Rakuten, a few referrals, and ordinary expenses. Within the next month, I expect that my wife and I will be back up to around 700,000 Membership Rewards points.

Ordinarily, that’s about the minimum number that I’d like to have on hand. People often ask about how many points are “enough” or how many are “too many”, which are questions that vary by situation. Personally, I like to have a healthy enough buffer so as to be able to find a backup plan if we get stuck needing a last-minute flight booking thanks to a cancelled flight or emergency change to a trip. Since we travel as a family of four and Amex points transfer to all of my favorite airline programs, I like having at least 700-800K points on hand for a “rainy day”.

However, it is widely expected that transfers from American Express Membership Rewards to Hawaiian Airlines Hawaiian Miles will end sooner rather than later. Tim recently reported on speculation that on June 30th may be a likely end date for that partnership, but Tim was also careful to caution that transfers could end at any time. Once that window closes, Alaska miles will once again be quite difficult to amass in a meaningful quantity.

We’ve currently got about 90,000 miles between Hawaiian and Alaska and I’ve got 120,000 coming soon enough from welcome bonuses for a total of 210,000. I feel like I should make another transfer from Amex to Hawaiian and on to Alaska, but the question is how much should I transfer? I’m nervous to transfer too many and risk being in a jam without enough transferable points, but I’m equally nervous about missing out on the chance to build up a meaningful balance of Alaska Mileage Plan miles!

The good news is that most of my favorite Amex transfer partners (in terms of airlines) are also Capital One transfer partners. I’ve built up a few hundred thousand Capital One miles, which eases the burden on my need to hold Amex points.

I’m leaning toward transferring 400,000 Membership Rewards points to Hawaiian and on to Alaska. That will give me just over 600,000 Alaska miles. While that’s a far cry from Greg’s big bet, it feels like a big gamble on my end since I’ll temporarily be running closer to empty than I’d like. Still, given that I’ll likely continue to have many ways to build up Membership Rewards points relatively quickly but relatively few ways to build up Alaska miles with any speed, I would be tempted to bump that up to 500K miles if I knew I could wait until late June to transfer (I’d prefer to wait until after a big trip ends in June before parting with more than 400K Membership Rewards points).

I do wish that we knew a certain end date for the Amex partnership. American Express charges an excise tax for transfers to US-based airline programs (there is no such fee for transfers to foreign airlines, nor does any other reward currency charge a fee for transfers to US-based airlines like Amex does). The fee maxes out at $99 per transfer. I’ve already made a couple of transfers to Hawaiian and paid the fee a few times in recent months, so I’d like to make one final transfer rather than transferring some now and some in June. However, to Tim’s point, transfers could end any day, so I likely won’t wait counting on a June end date. That means I’ll probably settle for a speculative transfer of 400K rather than paying to move miles twice.

Bottom line

It took me longer than it should have to dive all-in with Hawaiian Airlines miles. In recent months, I’ve booked flights between Europe and the US on Condor and between North and South American on LATAM for excellent value with Alaska Mileage Plan. The window of opportunity to quickly juice up one’s Alaska miles balance by collecting a large sum of Hawaiian miles is likely to be closing very soon and I’ve finally awoken to the opportunities that are living on borrowed time. While I certainly regret not getting in on the transfer bonus that Greg did last year and not getting the Hawaiian cards at better offers, I’m glad to get in before Hawaiian Miles are gone. Given my growing love of Alaska Mileage Plan miles, I think I am far more likely to regret not amassing even more Hawaiian Miles while I still could.

The post All-in with Hawaiian Airlines Miles: Better late than never? [2-card option is dead] appeared first on Frequent Miler. Frequent Miler may receive compensation from CHASE. American Express, Capital One, or other partners.